Error modeltime.h2o issue with modeltime_fit_resamples() #24

Description

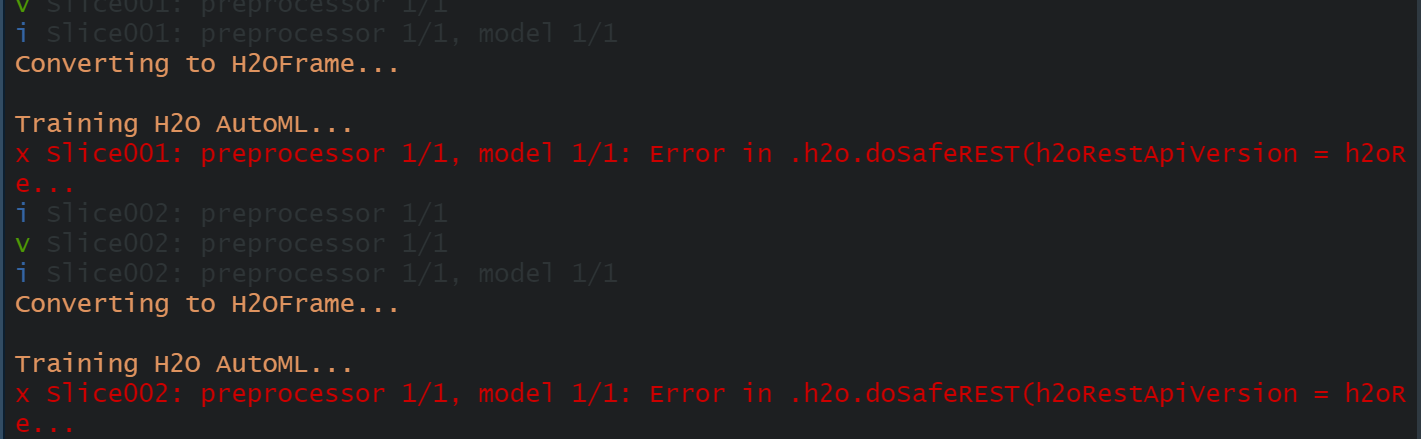

Hello @mdancho84, Here is reproducible codes for the error. I am using modeltime.h2o with modeltime resamples

library(Quandl)

Tidymodeling

library(modeltime.ensemble)

library(modeltime)

library(tidymodels)

Base Models

library(glmnet)

library(xgboost)

Core Packages

library(tidyverse)

library(lubridate)

library(timetk)

library(modeltime.h2o)

library(tidymodels)

library(h2o)

h2o.init()

h2o.removeAll()

df1 <- Quandl(code = "FRED/PINCOME",

type = "raw",

collapse = "monthly",

order = "asc",

end_date="2017-12-31")

df2 <- Quandl(code = "FRED/GDP",

type = "raw",

collapse = "monthly",

order = "asc",

end_date="2017-12-31")

per <- df1 %>% rename(PI = Value)%>% select(-Date)

gdp <- df2 %>% rename(GDP = Value)

data <- cbind(gdp,per)

data1 <- tk_augment_differences(

.data = data,

.value = GDP:PI,

.lags = 1,

.differences = 1,

.log = TRUE,

.names = "auto") %>%

select(-GDP,-PI) %>%

rename(GDP = GDP_lag1_diff1,PI = PI_lag1_diff1) %>%

drop_na()

horizon <- 6

lag_period <- 6

rolling_periods <- c(10:12)

data_pre_full <- data1 %>%

Add future window----

#bind_rows(

future_frame(.data = .,.date_var = Date, .length_out = horizon)

#) %>%

add lags----

tk_augment_lags(

.value = GDP : PI ,

.lags = lag_period)

%>%

add lag rolling averages

tk_augment_slidify(

.value = PI_lag6,

.period = rolling_periods,

.f = mean,

.align = "center",

.partial = TRUE)

2.0 STEP 2 - SEPARATE INTO MODELING & FORECAST DATA ----

data_prepared_tbl <- data_pre_full %>%

filter(!is.na(GDP)) %>%

dplyr::select(-PI) %>%

drop_na()

splits <- time_series_split(data_prepared_tbl, assess = 8, cumulative = TRUE)

recipe_spec <- recipe(GDP~ ., data = training(splits)) # %>%

train_tbl <- rsample::training(splits) %>% bake(prep(recipe_spec), .)

test_tbl <- rsample::testing(splits) %>% bake(prep(recipe_spec), .)

MODEL SPEC ----

model_spec <- automl_reg(mode = 'regression') %>%

parsnip::set_engine(

engine = 'h2o',

max_runtime_secs = 99999999999999999,

max_runtime_secs_per_model = 3600,

project_name = 'project_01',

nfolds = 0,

max_models = 2,

#exclude_algos = c("DeepLearning"),

include_algos = c("GLM"),

seed = 786

)

model_fitted <- model_spec %>%

fit(GDP ~ ., data = training(splits))

leaderboard <- automl_leaderboard(model_fitted)

leaderboard

model2 <- leaderboard$model_id[[1]]

model_fit_2 <- automl_update_model(model_fitted, model2)

MODELTIME ----

calibration_tbl <- modeltime_table(

model_fit_2)

resample_spec <- rolling_origin(

data_prepared_tbl,

initial = 100,

assess = 6,

cumulative = TRUE,

skip = 0,

lag = 0,

overlap = 0

)

resamples_fitted <- calibration_tbl %>%

modeltime_fit_resamples(

resamples = resample_spec ,

control = control_resamples(verbose = TRUE))

resamples_fitted %>%

modeltime_resample_accuracy(

metric_set = metric_set(rmse, rsq))